Global Cyber Risk Report stands alone in its ability to help businesses make better cyber risk decisions thanks to the unique way we have drawn together data and interpretation across critical cyber security controls, cyber events and the cyber insurance market — globally and by region. Beinsure analyzed the report and highlighted the key points.

Amid escalating cyber risk, Aon’s Cyber Quotient Evaluation (CyQu), our patented global assessment platform, delivered a positive outlook from our responders and showed that companies are overall maturing.

This proved to be particularly true for our enterprise clients. Understanding the need to align cyber insurance to cyber security strategy became more prevalent among large companies, where we also saw greater collaboration across stakeholders, up and down the organization.

Third-party risk continued as a frontline issue across the year, as businesses found it increasingly challenging to protect their supply chains.

And importantly, we observed occasional misunderstandings about what cyber insurance covers – and doesn’t cover — which reflects the need for more education across the industry (see U.S. Cyber Insurance Premium Rates).

Cyber Claims Rise. Payouts Decline

As cyber attacks persisted, the frequency of cyber claims grew across 2024, ranging from ransomware and business interruption to class action litigation and regulatory investigations — resulting in an increasingly complex incident response.

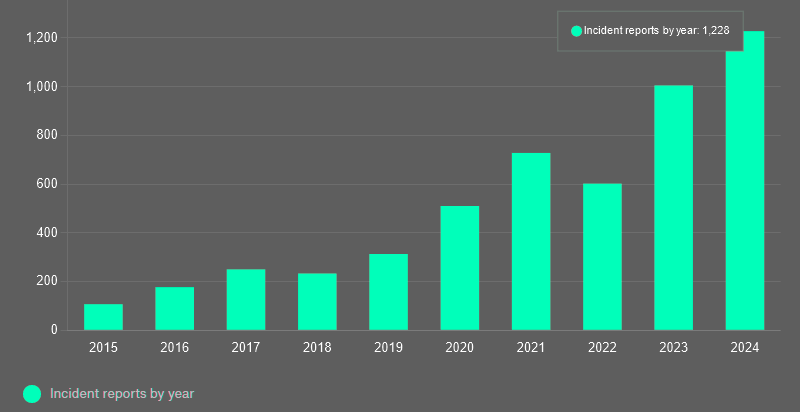

In the U.S., for example, Aon Cyber and Errors and Omissions (E&O) claims data revealed 1,228 reported incidents across broking clients in 2024, reflecting an increase of 22% year over year.

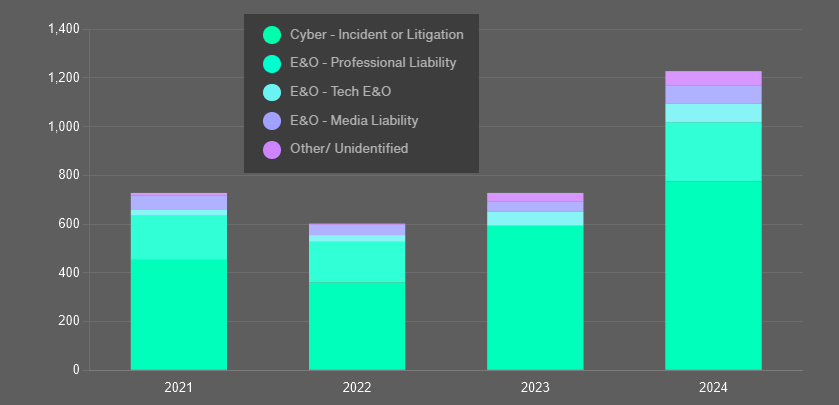

Cyber events or litigation represented most claims, with 776 reported matters in the U.S. — up a third on the previous year — and 320 reported matters in EMEA.

U.S. E&O-Cyber Broking Reported Incident

This increase was driven by a rise in cyber incidents, more organizations acquiring cyber insurance and a heightened regulatory focus on publicly disclosing material events.

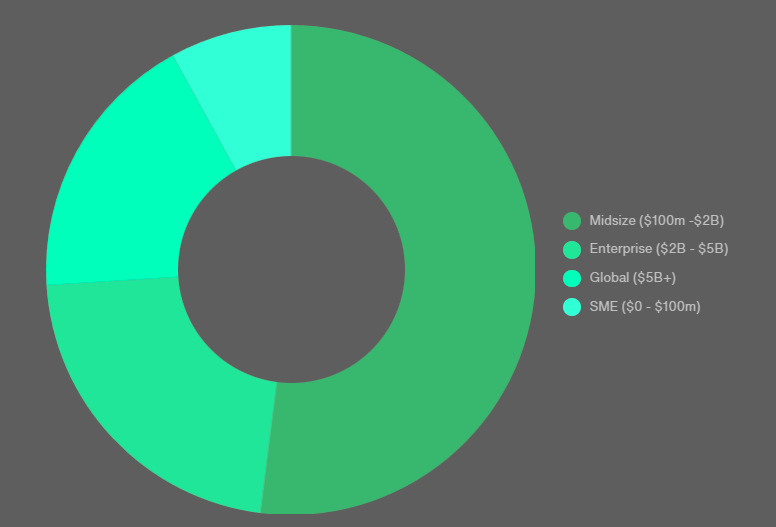

Midsized organizations with $100 mn to $2 bn annual revenue filed more claims than any other group, representing 52% of all matters, according to Cyber Insurance Market Outlook for 2024-2034.

Aon analysts observed underinsurance and a lack of basic cyber readiness plans exposed mid-market organizations to significant risk.

U.S. E&O-Cyber Broking Reported Incidents

Response plans enable organizations to reduce the cost of a breach by an average of almost $500,000, providing reassurance about the effectiveness of these strategies.

Ransomware Persists

Ransomware incidents persisted in 2024, increasing 24 percent versus 2023. Fraud and social engineering remained flat while claims frequency for privacy and data breaches and lost, missing, or stolen data decreased.

Ransomware payment bans are back on the table as governments contemplate minimizing payments and compelling cybercriminals to cease attacking their countries’ organizations.

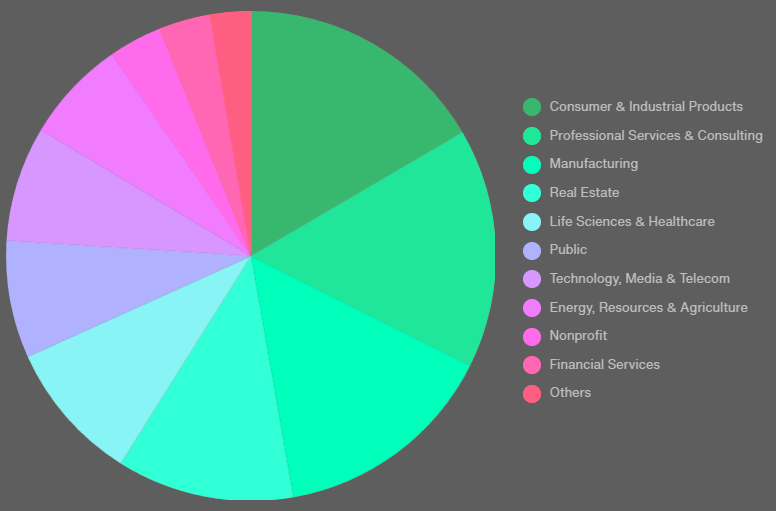

Ransomware Victims by Sector

Access claims trended up and down across the year. Access claims arise when threat actors, known as initial access brokers, breach organizations’ networks and sell this unauthorized access to other threat actors, leading to ransomware attacks and malicious activities.

Cyber Risk Insurance Market

Significant, systemic events dominated 2024 with Aon’s Cyber Solutions U.S. data revealing 1,228 reported incidents across Aon’s Cyber Solutions clients — an increase of 22%. Cyber incidents or litigation represented most claims, with 776 reported incidents — up 31%.

Despite increased claims frequency in 2024, insurer loss ratios were not materially impacted, and buyers’ market conditions continued through 2024 for cyber amid a well-capitalized and competitive environment.

Favorable conditions are expected to continue in 2025, supporting growth in emerging cyber markets; however, the juxtaposition of loss trends and a softening market could mean future market volatility. Risk differentiation remains key to favorable renewal outcomes over the long term.”

On average, buyers achieved a 7% premium decrease in Q1 2025, primarily driven by ample capacity, the introduction of new capacity and incumbent insurers being aggressive with renewal terms to maintain their incumbent renewals.

The cyber insurance and reinsurance markets maintained solid margins, reinforcing the view that the global cyber sector remains stable despite increased competition and the growing frequency, severity, and sophistication of cyber events.

Competitive pressure has resulted in lower self-insured retentions, reduced premiums, eased sub-limit requirements, and broader policyholder coverage.

Pricing is expected to continue moderating through 2025, with improving conditions across more risk profiles and regions. Despite elevated ransomware activity in previous years, a buyers’ market persists due to available capacity and strong competition. Most markets now offer moderate rate reductions, expanded coverage, and higher limits for risks supported by effective cybersecurity controls.

FAQ

The Global Cyber Risk Report stands out by integrating data across cybersecurity controls, cyber incidents, and cyber insurance markets globally and regionally. Its strength lies in providing actionable insights by connecting technical security maturity with insurance coverage trends and risk outcomes.

Businesses, especially large enterprises, are maturing in cyber risk management. Aon’s CyQu platform revealed improved cyber posture among respondents. There’s also a growing trend to align cybersecurity strategies with cyber insurance planning, driven by better internal collaboration across departments and executive leadership.

Third-party risk remains a top concern due to the complexity of managing supply chain vulnerabilities. Organizations find it increasingly difficult to ensure vendors and partners meet cybersecurity expectations, making them susceptible to indirect breaches through poorly secured third-party systems.

Cyber claims rose significantly in 2024, with Aon reporting a 22% year-over-year increase. Ransomware remained the dominant incident type, with a 24% rise from 2023. Midsized firms ($100M–$2B revenue) filed the most claims, often due to underinsurance and lack of robust response plans.

Despite the surge in cyber claims, the market remains stable and competitive. In Q1 2025, buyers saw a 7% premium decrease, with expanded coverage and improved terms. This “buyers’ market” is supported by strong insurer capitalization and aggressive pricing strategies. However, potential future volatility exists due to rising attack sophistication and loss trends.